| Monthly Market Analysis September 2025 |

Economy

Tariffs

On August 29th a U.S. Federal Appeals court upheld that the Trump tariffs enacted under the the International Emergency Economic Powers Act (IEEPA) are not authorized, prompting the Trump administration to make a request to the U.S. Supreme Court for a dismissal of the U.S. Appeals court ruling. The U.S. Supreme court agreed to hear the case on November 5th, with their decision likely being rendered many months following the hearing.

Trump’s Tariffs Note:

Tariffs on American imports are expected to increase the price of goods for American consumers and cut into the profits of American businesses. Nevertheless, the Trump administration has decided to utilize import tariffs to achieve their priorities:

- Tariffs are being implemented to encourage companies to manufacture their products in the United States. The Trump administration expects that companies will eventually produce their products in the United States to avoid tariffs.

- The revenue from tariffs will be used to help pay for the One Big Beautiful Bill Act, passed on July 4th, 2025. The One Big Beautiful Bill act extends expiring tax reduction legislation, which was originally enacted in 2017 during Donald Trump’s first administration, along with other Republican Party priorities. The Congressional Budget Office estimates the cost of extending the 2017 tax cut legislation for ten additional years will be over $4 Trillion Dollars.

- Tariffs on U.S goods are being implemented to help eliminate the American trade deficit with other countries. The U.S. tariffs will be used as leverage to coerce other countries to lower their own tariffs and non-tariff barriers.

- Tariffs are being used as punishment for countries that refuse to carry out American demands on a range matters unrelated to trade.

Trump’s Tariffs Implemented in 2025

- 35% tariff on Canadian Goods (Except goods covered under the Canada-United States-Mexico trade agreement). Canada is still negotiating lower rates and has implemented counter tariffs.

- 30% tariff on Chinese goods. Negotiation deadline has been extended.

- 15% tariff on Japanese goods. Trade deal framework agreed upon

- 10% tariff on United Kingdom goods. Trade deal framework agreed upon.

- 15% tariff on European Union goods. Trade deal framework agreed upon.

- 50% tariff on Indian goods.

- 25% tariff on Mexican Goods (Except goods covered under the Canada-United States-Mexico trade agreement). Negotiation deadline has been extended.

- 50% tariff on all iron, steel and aluminum imports into the United States except for the United Kingdom and Russia which are tariffed at 25% and 200% respectively.

- 50% tariff on copper imports into the United States.

- 25% tariff on automobiles and automobile parts into the United States, except for the United Kingdom and the European Union which are tariffed at 10% and 15% respectively.

- 10% tariff on all Canadian energy imported into the United States that is not covered under the Canada-United States-Mexico trade agreement.

- 10% tariff on all Canadian and Mexican potash imported into the United States that is not covered under the Canada-United States-Mexico trade agreement.

- 10% – 41% tariffs on all other trading partners based on the size of their trade deficit with the United States.

Conditions under which Trump’s Tariffs will be Lowered or Eliminated

- Legal: Trump’s tariffs mostly contravene international trade law, but enforcing these laws can be a long, tedious process often with no enforceable remedies. American industries that are impacted by Trump’s tariffs often have lobby groups that can challenge the legality of the Trump’s Tariffs in U.S. courts. The United States Congress could also intervene, since tariffs are typically under their purview, but Republicans have a majority in Congress and are unlikely to move against their party leader.

- Political Backlash: The negative impact of higher consumer prices in the United States and/or the unavailability of needed/desired goods due to retaliatory actions taken by other countries may generate political backlash from U.S. consumers and businesses.

- Trade Negotiations: At any time, trade negotiations between the United States and its trading partners around the world could lower or eliminate the newly enacted tariffs.

- U.S. Midterm Elections: In November 2026, U.S. Congressional Elections may change the political environment. If American voters are unhappy with how the Trump’s Tariffs are impacting their lives, Republicans could lose their majority in Congress.

- Four Year Presidential Term: In less than four years Donald Trump will complete his second and final term as the President of the United States of America. A newly elected American President could undo the Trump’s Tariffs, if they are still in place.

* The legality of Trump’s Tariff’s enacted under the International Emergency Economic Powers Act (IEEPA) are scheduled to be heard by the U.S. Supreme Court on November 5, 2025, but it will likely be many months before they render a final ruling on the case.

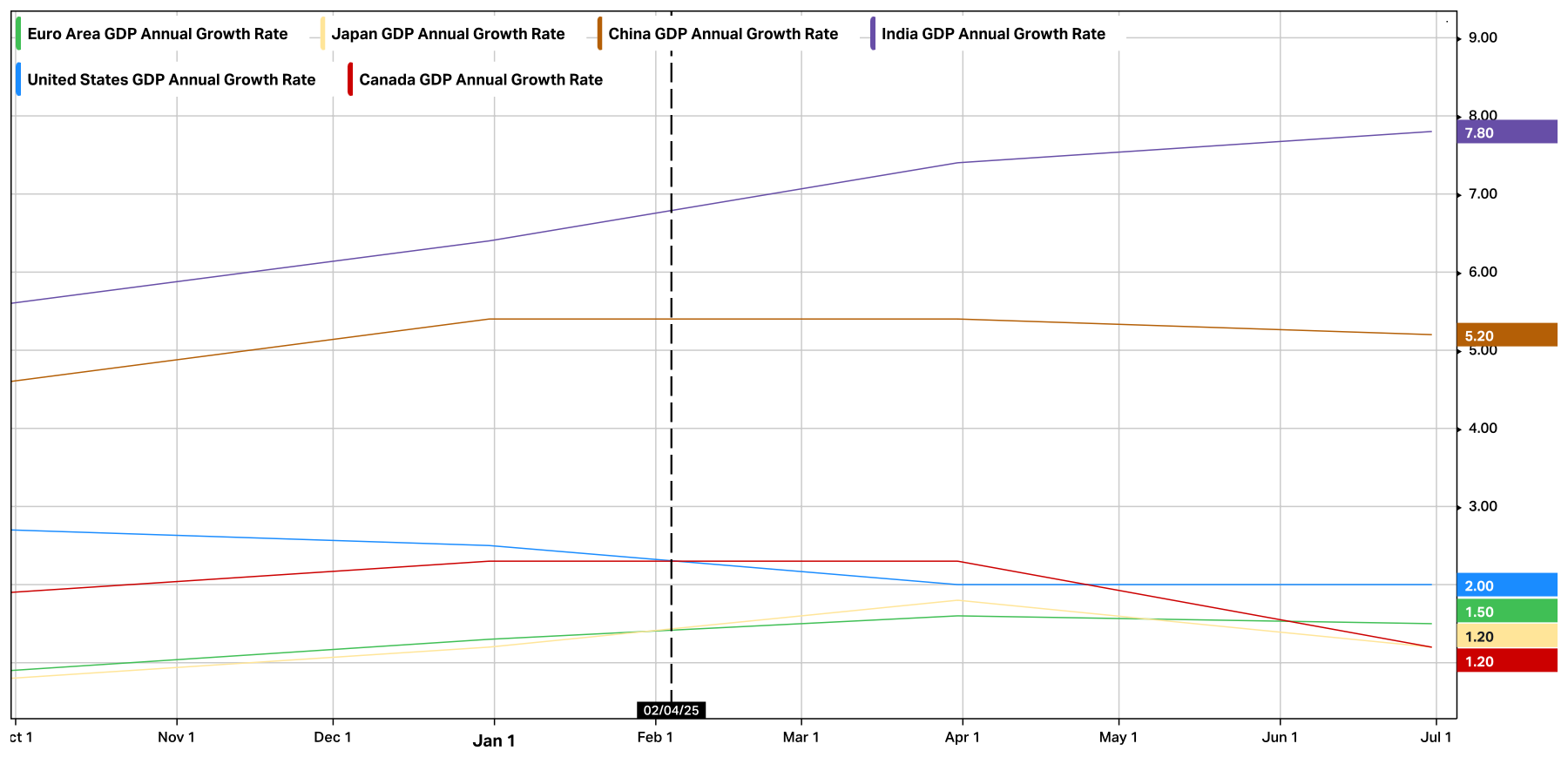

Global Economic Growth (Annual GDP Growth Rate) After Trump’s Tariffs – 1 Year Chart

Declining Economies

| Economic Decline after Trump’s Tariffs | |

| United States | -0.5% |

| Canada | -1.1% |

| China | -0.2% |

| Japan | -0.1% |

Global Annual GDP Growth Rates after Trump’s Tariffs (beginning February 4th):

The U.S. economy’s (blue) annual growth rate declined from 2.5% to 2.0%. The Canadian economy’s (red) annual growth rate declined from 2.3%. to 1.2%. China’s annual economic growth rate (brown) fell from 5.4% to 5.2%. The Eurozone’s annual economic growth rate (green) increased from 1.2% to 1.5%. The Japanese annual economic growth rate (yellow) declined from 1.30% to 1.20%. India’s annual economic growth rate (purple) increased from 6.4% to 7.4%

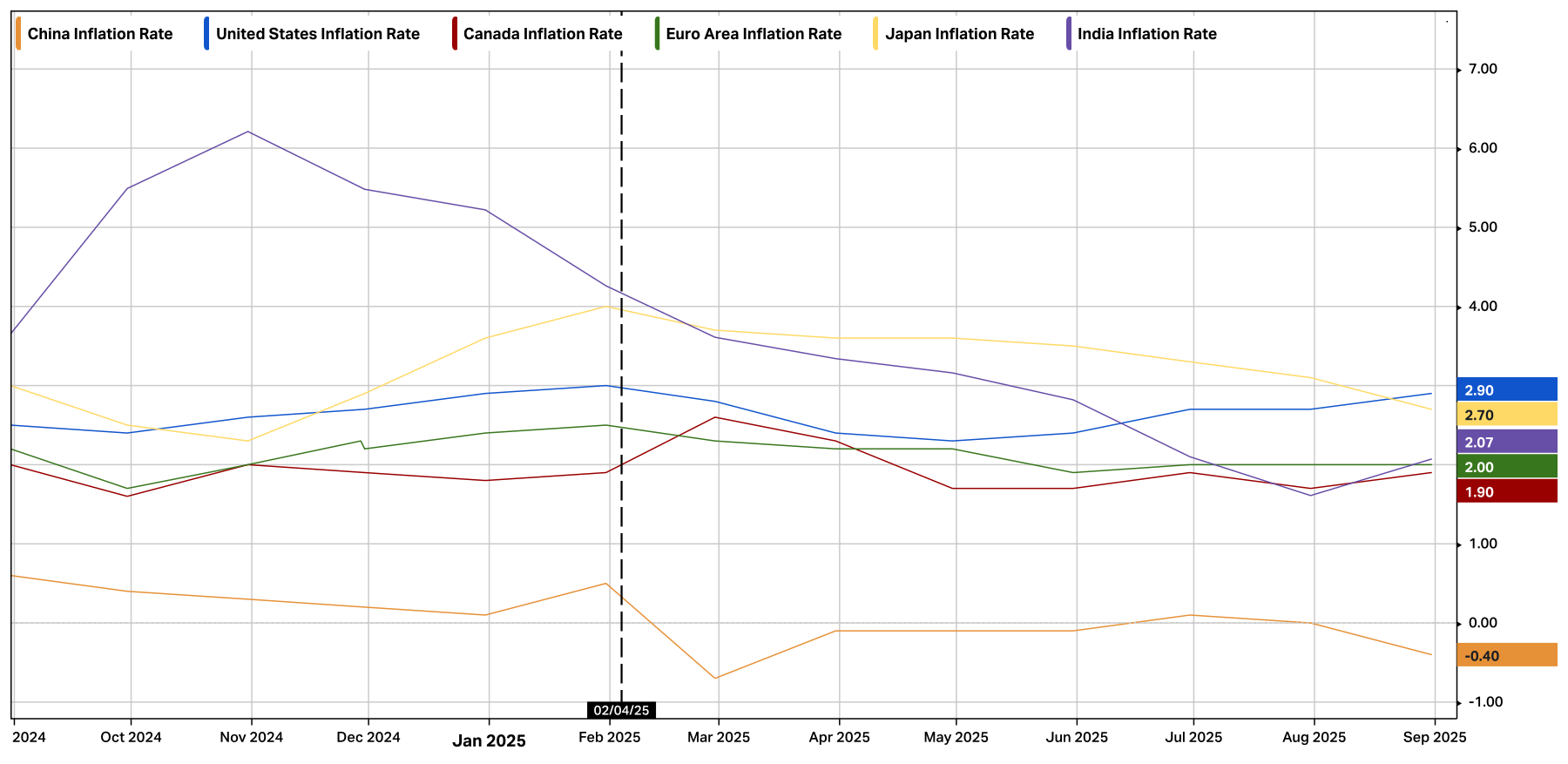

Global Inflation Rates (Annualized) After Trump’s Tariffs – 1 Year Chart

Global Annual Inflation Rates after Trump’s Tariffs (beginning February 4th):

Since Trump’s Tariffs were implemented the inflation rate for all the tracked economies have moved lower except Canada. Canada’s inflation rate (red) is unchanged at 1.9%. The United States’ inflation rate (blue) declined from 3.0% to 2.9%. The Eurozone inflation rate (green) fell from 2.5% to 2.0%. China’s inflation rate (brown) declined from 0.5% to -0.4%. Japan’s inflation rate (yellow) fell from 4.0% to 2.7%, and India’s inflation rate (purple) fell from 4.26% to 2.07%.

United States

In August the American economy generated a mere 22,000 jobs, providing further evidence of a slowing U.S. labour market. A revision of previously stated labour market data revealed that the U.S. economy lost -13,000 jobs in June, the first decline in monthly jobs since December 2020. On October 3rd, we will find out if the trend of tepid job growth in the United States continues, when we get the U.S. Bureau of Labour Statistic’s jobs report for September. The U.S. unemployment rate increased from 4.2% to 4.3% in August, its third consecutive move upwards.

During the month of August, American consumers continued spending as retail sales increased by 0.6%. The continued improvement in retail sales has contributed to higher consumer prices. The U.S. inflation rate jumped from 2.7% to 2.9% in August, lead by rising food and used car prices.

Rising inflation and weak job growth made the decision to cut rates more difficult for U.S. Federal Reserve. On one hand lower interest rates would help the job market by making it less expensive for businesses and consumers to borrow, but on the other hand the possible increased spending from lower rates could push the demand for goods higher, leading to higher inflation. The U.S. Federal Reserve determined that the risk of a weak job market was a more important consideration than rising inflation as they decided to cut interest rates by 0.25% in their meeting on September 17th.

Canada

For the second month in a row the Canadian economy lost a massive amount of jobs. After losing -40,800 jobs in July, Canada lost an additional -65,500 jobs in August. According to Statistics Canada the job losses were concentrated in professional, scientific, and technical services, as well as the manufacturing sector. In August, the unemployment rate rose from 6.9% to 7.1%, providing additional evidence of a weak Canadian labour market.

On a positive note, preliminary data from Statistics Canada revealed that Canadian consumers continued spending as retail sales rose 1% in August after falling -0.8% in July.

Canada’s inflation rate reversed it’s downward trend in August; it rose from 1.7% to 1.9%. The higher inflation reading was primarily driven by rising food prices.

The Bank of Canada decided that inflation is less of a concern and put their focus on the deteriorating job market as they cut interest rates by 0.25% in their meeting on September 17th.

Markets

Global Stock Markets

The Canadian and U.S. stock markets had another positive month in August as investors were less concerned with tariffs and more enthusiastic about expected interest rate cuts.

During the month of August, the U.S. Market (S&P 500) was up 1.91%, while the Canadian market (S&P/TSX Composite Index) was up an astronomical 4.79%. The U.S. Nasdaq Composite index which contains a high weighting of technology related stocks was up 1.58% as investors look for additional opportunities in other sectors of the market. The German stock market (Dax 40 index) decreased by -0.68%, while the Chinese market (Shanghai Composite Index) grew by 7.97% and the Indian market (Nifty 50 Index) was down -1.38%.

Change in Global Stock Markets the Month of August 2025

The recent interest rate cuts (September 17th) by both the Bank of Canada and the U.S. Federal Reserve has provided encouragement for stock market investors. Many market participants are expecting additional interest rate cuts this year. The conundrum for investors is that inflation has been on an upward trajectory in both Canada and the United States, which may cause the Bank of Canada and the U.S. Federal Reserve to pause their rate cuts. Of course a weak labour market is also of great concern to Canadian and American central bankers. Therefore we will have to pay attention to the magnitude of any rise in inflation or weakness in job growth to determine the eventual path of interest rates. Given the high expectation of market participants for additional rate cuts, inflation and jobs data will be of upmost importance in determining market performance over the next few months.

| 1 (Source: Bank of Canada) 2(Source: Statistics Canada) 3(Source: United States Bureau of Labour Statistics) 4(Source: United States Federal Reserve) 5(Source: United States Census Bureau) 6(Source: FactSet as of August 29, 5:00 PM) * This information has been prepared by Desmond Rubie, BCom, FCSI®, CIM®, CFP®, who is a Wealth Advisor for Rubie Wealth Management Group at iA Private Wealth. Opinions expressed in this article are those of Desmond Rubie, BCom, FCSI®, CIM®, CFP® only and do not necessarily reflect those of iA Private Wealth Inc. *IA Private Wealth Inc. is a member of the Canadian Investor Protection Fund and the Canadian Investment Regulatory Organization. iA Private Wealth is a trademark and business name under which iA Private Wealth Inc. operates.  Desmond Rubie, BCom, FCSI®, CIM®, CFP® Wealth Advisor Rubie Wealth Management Group | iA Private Wealth Insurance Advisor | iA Private Wealth Insurance* 26 Wellington Street East, 2nd Floor, Toronto, ON M5E 1S2 T: 647-429-3281 ext. 240018 Desmond.Rubie@iaprivatewealth.ca Schedule a Meetingrubiewealth.com Fellow of CSI (FCSI®) iA Private Wealth Inc. is a member of the Canadian Investor Protection Fund and the Canadian Investment Regulatory Organization. iA Private Wealth is a trademark and business name under which iA Private Wealth Inc. operates. *Insurance products are provided through iA Private Wealth Insurance, which is a trade name of PPI Management Inc. Only products and services offered through iA Private Wealth Inc. are covered by the Canadian Investor Protection Fund. |

Leave a Reply